“What does it mean for VfM if we have all of our costs of change upfront: but see ongoing benefits later? Isn’t there an effect of discounting on this pattern?”

There are always really good questions that come up on my VfM training courses. I have decided to record some of my responses to them as blog posts so that anyone interested can benefit from the insightful questions and (hopefully) useful responses.

If you are interested in my training please look at the core course details here and the module information here. Booking links are also on the website.

The training is delivered using an online hybrid model of on-demand videos with a live session for Q&A and deepening the knowledge. There is a core course introducing VfM and three modules on VfM and evaluation, VfM under complexity and one on cost-benefit analysis and benefit:cost ratios.

This question is a great one because it is something that everyone encounters, but it has some nice technical elements relating to the effects of discounting.

I give a full explanation of discounting costs and benefits over time in the VfM training CBA module, but basically it allows for the inescapable and evidence-based fact that individuals (and by extension entities made up of people) prefer to have money now rather than money in the future.

As a result, money in the future is valued less.

So, when money in the future is valued less it makes a difference when your costs arise compared to your benefits. Big up-front investments cost you now or very soon. So they don’t get reduced much in the discounting process.

But your ongoing stream of benefits, say running 20 years into the future, get discounted a bit more every year and so they are worth less and less as they stream into the future.

So it doesn’t take too much to visualise that, even with the same headline cost, your pattern with upfront investment needs considerably more future benefits to offset.

The other pattern is that you have costs every year and benefits every year. This means that your costs are getting reduced at the same rate as your benefits. As they march hand in hand they both get discounted at the same rate and so you don’t need as much benefit to offset the costs.

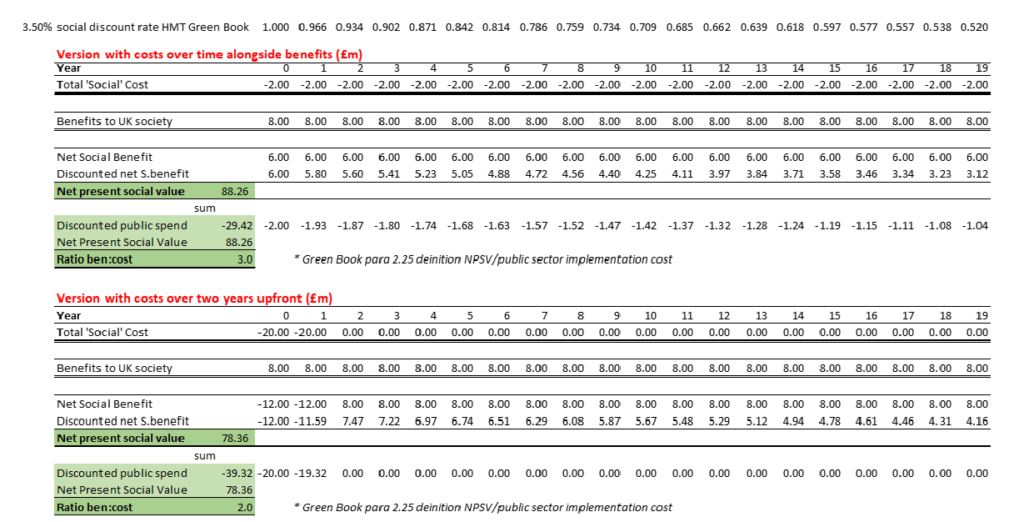

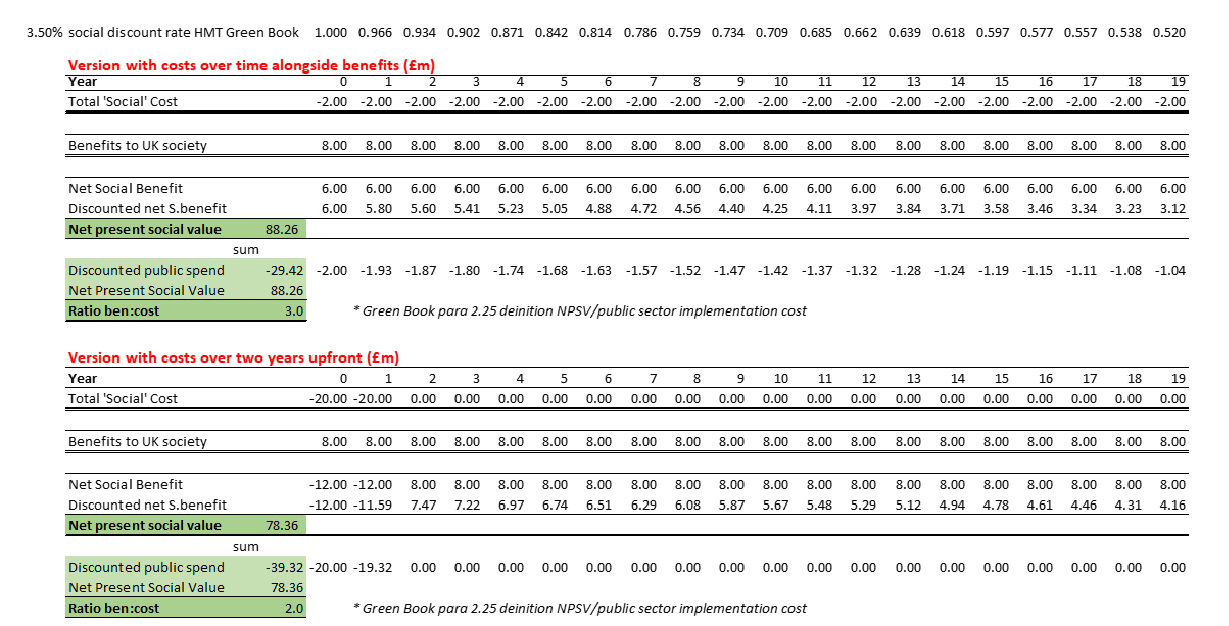

Here’s the spreadsheet that shows that… you can see that the headline benefit:cost ratio drops from about 3 to about 2 when you change the costs from arising equally every year to seeing them all sit in the first two years.

{kind=link}

I thought that was a great question and an interesting point. You can argue for yourself how the standard CBA approach feels in the reality of an example you know. Does this reflect how VfM really feels like it works in the wild? Would you instinctively think of things this way of you were doing a VfM assessment comparing the two cases of how costs arise without a formal CBA…?

Don’t forget to sign up for my VfM training if you haven’t been on it already – and please tell your friends and colleagues if you think they will be interested.

Thanks – and please get in touch if you would like to talk about anything around VfM, your strategy and evidence and how I may be able to support you in your work.